Completed

1:01:33 LOS: Describe how currency swaps are priced and calculate and interpret their no-arbitrage value.

Class Central Classrooms beta

YouTube videos curated by Class Central.

Classroom Contents

Pricing and Valuation of Forward Commitments - 2025 Level II CFA Exam Derivatives Module 1

Automatically move to the next video in the Classroom when playback concludes

- 1 0:00 Introduction and Learning Outcome Statements

- 2 6:55 LOS: Describe the carry arbitrage model without underlying cashflows and with underlying cashflows.

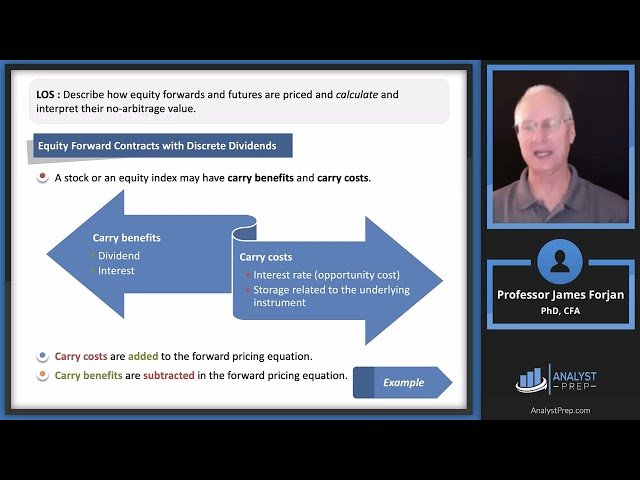

- 3 22:16 LOS: Describe how equity forwards and futures are priced and calculate and interpret their no-arbitrage value.

- 4 31:32 LOS: Describe how interest rate forwards and futures are priced and calculate and interpret their no-arbitrage value.

- 5 43:49 LOS: Describe how fixed-income forwards and futures are priced and calculate and interpret their no-arbitrage value.

- 6 49:40 LOS: Describe how interest rate swaps are priced and calculate and interpret their no-arbitrage value.

- 7 1:01:33 LOS: Describe how currency swaps are priced and calculate and interpret their no-arbitrage value.

- 8 1:04:15 LOS: Describe how equity swaps are priced and calculate and interpret their no-arbitrage value.