Completed

Full replication

Class Central Classrooms beta

YouTube videos curated by Class Central.

Classroom Contents

Liability-Driven and Index-Based Strategies for Fixed-Income Portfolio Management - Part 2

Automatically move to the next video in the Classroom when playback concludes

- 1 Introduction

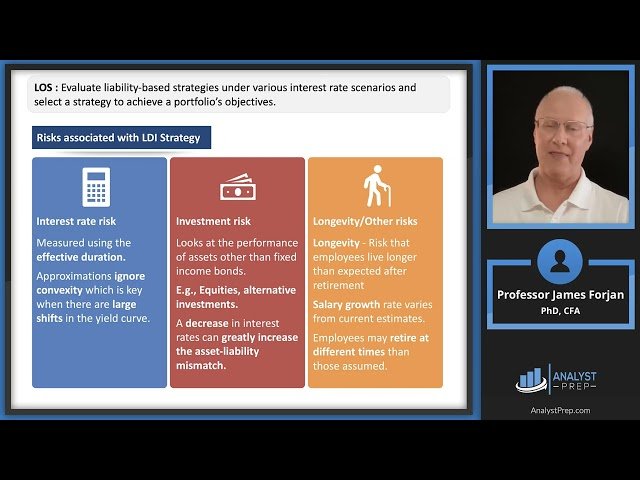

- 2 LiabilityDriven Investing

- 3 Measuring Retirement Benefits

- 4 Effective Duration Formula

- 5 Duration Gap

- 6 Number of Futures Contracts

- 7 SW Options

- 8 Airline Story

- 9 Model Risk

- 10 Spread Risk

- 11 Indexing

- 12 Duration convexity relationship

- 13 Full replication

- 14 Total return swaps

- 15 Enhanced indexing

- 16 Callable bonds

- 17 Policy statement

- 18 Bums

- 19 Recap