Completed

Estimating Market Risk Measures (FRM Part 2 2025 – Book 1 – Chapter 1)

Class Central Classrooms beta

YouTube videos curated by Class Central.

Classroom Contents

FRM Part 2 - Book 1 - Market Risk Measurement and Management

Automatically move to the next video in the Classroom when playback concludes

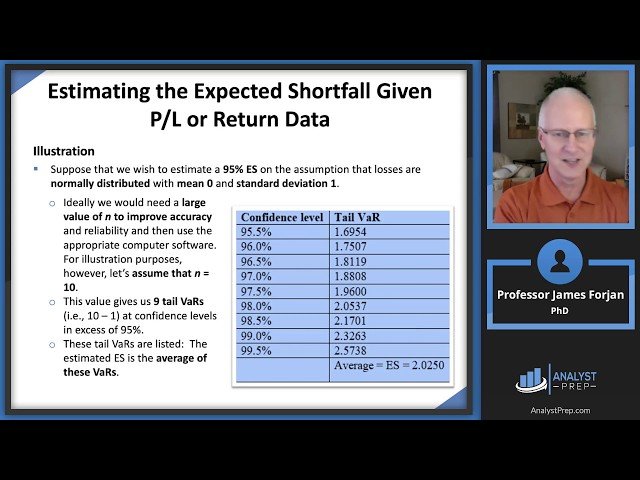

- 1 Estimating Market Risk Measures (FRM Part 2 2025 – Book 1 – Chapter 1)

- 2 Non-Parametric Approaches (FRM Part 2 2025 – Book 1 – Chapter 2)

- 3 Parametric Approaches (II): Extreme Value (FRM Part 2 2025 – Book 1 – Chapter 3)

- 4 Correlation Basics: Definitions, Applications, and Terminology (FRM Part 2 – Book 1 – Chapter 7)

- 5 Empirical Properties of Correlation: How Do Correlations Behave in the Real World? (FRM P2–B1–Ch8)

- 6 Financial Correlation Modeling – Bottom-Up Approaches (FRM Part 2 2025 – Book 1 – Chapter 9)

- 7 The Science of Term Structure Models (FRM Part 2 2025 – Book 1 – Chapter 11)

- 8 The Art of Term Structure Models: Drift (FRM Part 2 2025 – Book 1 – Chapter 13)

- 9 The Art of Term Structure Models: Volatility and Distribution (FRM Part 2 – Book 1 – Chapter 14)

- 10 Volatility Smiles (FRM Part 2 2025 – Book 1 – Chapter 15)

- 11 CFA® Exam, FRM® Exam, and Actuarial Exams Video Lessons offered by AnalystPrep